Investment Idea - Creightons PLC (XLON:CRL)

Investment Idea - Creightons PLC (XLON:CRL)

Interesting microcap in a defensive sector and well managed

HISTORY AND INTRODUCTION

Creightons Plc was registered in 1975 to continue the business of manufacturing and marketing toiletries made exclusively from natural products first established in 1953. It created a number of proprietary brands, although it focused mainly on private label and contract manufacturing.

The Group consolidated its manufacturing at the Potter and Moore Innovations plant in Peterborough following the acquisition of the Potter and Moore business in 2003 and disposal of the Storrington site in 2005. The Group acquired the business and assets of the Broad Oak Toiletries site in Tiverton in February 2017 further increasing the Group’s sales reach in terms of product and premium customers and adding to manufacturing capability and capacity. In June 2019 the Group bought the Balance Active Formula brand.

It was listed in the London Stock Exchange in 1987. It is an unknown microcap, capitalises 57 GBP millions and no analyst coverage.

It has shown resilience in crisis periods, management has done a nice job with good capital allocation and “skin in the game”.

SECTOR

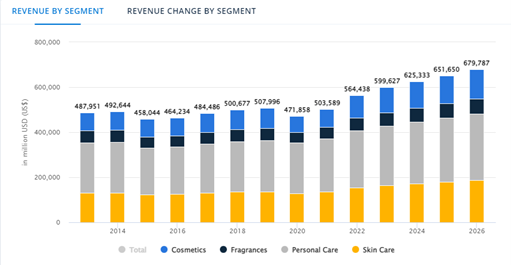

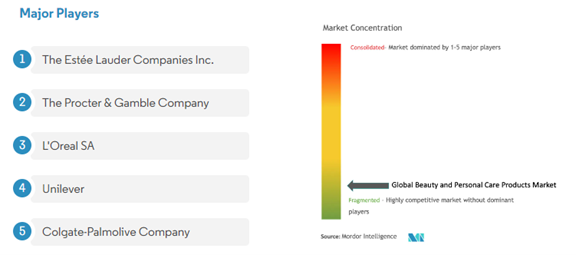

The “Beauty & Personal Care” market is relatively mature although it is constantly evolving as brands seek to differentiate their offering in order to generate sales opportunities, it is a fragmented market and highly competitive. However, there are several big players who have high brand recognition and global presence, we are talking about brands that we see in our day-to-day: L`Oreal, P&G, Unilever, Estée Lauder…

According to Statista “Beauty and Personal Care” industry is expected to grow by 5% annually in coming years.

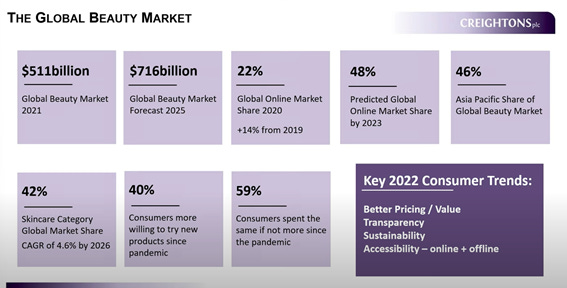

In the last few years there has been a heightened interest in premium products through online channels driven by digital advertisement via social networks (Instagram and Tik Tok mainly.). Furthermore, the market has seen a growing demand for beauty products fabricated by organic components and non-chemical substances.

In each Creighton´s earnings presentation, Marketing Director “Philippa Clark” shares her impressions about the industry and situation of the global beauty market.

BUSINESS

The Group’s operations are organized into three business streams:

• OWN BRANDED BUSINESS (12 M Sales in 2021): which develops, markets, sells and distributes products Creightons has developed and own the rights to or brands it has licensed. These sales are increasingly made direct to consumers. They are betting hard for this segment; the company is increasing brand portfolio under management, and it,s focusing on high quality products. They plan to achieve 40M sales in 2024 through this segment.

• PRIVATE LABEL BUSINESS (22,7 M Sales in 2021): which focuses on high quality private label products for major high street retailers and supermarket chains (ALDI, TESCO…), with most of the stock manufactured to forecast. This kind of business line is usually characterized by low margins. One important point to take into consideration is that the company has improved client diversification, it was very dependent on Tesco concentrating more than 40% of sales in the past, and now has a wide portfolio of clients with no customer concentration.

• CONTRACT MANUFACTURING BUSINESS (12,3M Sales 2021): which develops and manufactures products on behalf of third-party brand owners and typically manufactured to order. Additionally, the company helps these brands in other value addition activities such as design or consulting. Management expects good future in this business line, the company has a good position and clients recognize Creighton´s know-how.

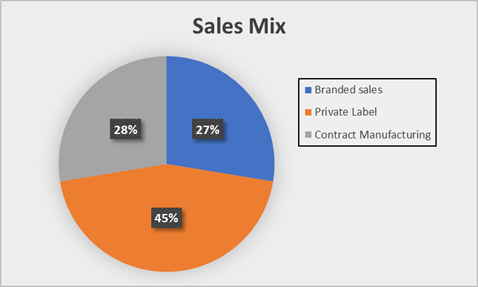

Sales breakdown by business stream in the last earnings release was as follow:

The company has been awarded with many “Global Makeup Awards” thanks to the votes of general public, so we can assume that the products have a well-known quality, important aspect in this industry and a key point to consider in microcap companies.

Generally, reviews available in Amazon are positive.

Regarding business stream “Own Branded”, in 2021 the company acquired “EMMA HARDIE”, this brand offers premium products providing higher margins than mass or masstige brands. Additionally, EMMA HARDIE is really focused on online channels as 50% of sales are done through this channel. The acquisition was financed by share issuance and cash.

Management hope to achieve 25 million of online sales at the end of 2024, so the company is focusing on boost sales through online channels (1,4M in 2021). As we can see in the next slide, they are well positioned selling its products on well-known channels.

FINANCIALS

Creightons has increased its revenues 11,5% CAGR from 2005 to 2021, they just suffered a decreased in revenues in two years (2009 and 2010) corresponding to financial crisis periods.

Margins have improved considerably in last years, always keeping in mind that we aren’t talking about a software firm characterized by high margins. We could see an improvement in margins if the company continues driving to premium products with better margins and online sales, as they defined in the strategic plan.

During CO-VID19 crisis, the company sold 14,6M through hydroalcoholic gel (one-off sale), in the last months the company has replaced this one-off sale by growth in each of the three business streams offsetting the loss of the “one off” hygiene sales over the same period in the previous year.

The main distribution region is UK (over 80% of sales), one of the company objectives is to increase overseas sales.

Cash conversion cycle has had a downward trend in last years, however, there has been an increase in last months. It´s a point to bear in mind and control in coming quarters.

Financial situation is healthy, it has never been too indebted and used to have net cash position. Currently, it has 0,4 net debt/EBITDA ratio, low debt.

It is not a capital-intensive business, we can estimate maintenance capex around 1% of sales and total capex is expected to be around 3-4% in coming years according to management comments.

ROIC has been around 20% in recent years.

They have issued shares (2,4% CAGR in last 5 years) in order to pay for acquisitions and to pay stock options. We can assume that it is not an excessive dilution, but it is a point to consider in our valuation.

MANAGEMENT

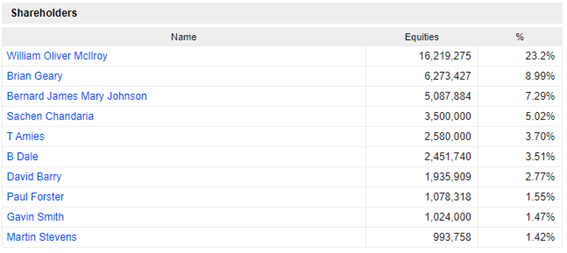

We have an experienced management with strong background in the industry that has driven the company in the right direction considering a highly competitive enviroment, adding value via M&A and understanding market needs at the same time that are directing the company to better financials and margins. The vast majority of executives hold a huge quantity of shares and the chairman owns 23% of the company. Management is aligned with shareholders, which is a key point in a microcap company as Creightons.

The company distributes a dividend of 0.15p per ordinary share (Around 1% Dividend Yield).

They expect to reach 100 million sales and EBITDA margin of 12,5% in 2024 according to the existing strategic plan. Management is confident in achieve these goals and they hope to do it through a mix of organic and inorganic growth. Bernard commented in last conference call that they expect grow 20M organically and 20M via M&A.

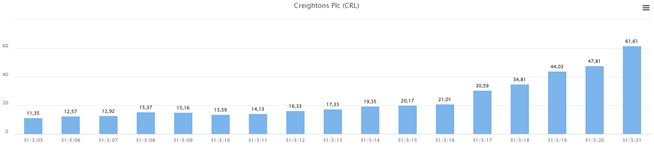

Stock performance has been exceptional in last years, it has been appreciated by 41,6% per year in last 10 years. However, the stock follows a downward trend from summer 2021 when it reached all-time highs, almost a 50% drop since then, but, there is no relevant news that affect company fundamentals, just market volatility, normal events in illiquid microcaps.

RISKS

Before going to valuation, let´s see some potential risks.

· Country risk: The company is listed and makes most of its sales in the United Kingdom. In the event of bad news, the price could suffer due to the small size of the company and the current negativity in the British market.

· Production problems: In the past, the company had problems to cover existing demand, which is why the stock was punished in 2018, however, it seems that it is already a lesson learned.

· Competition: The company belongs to a fragmented and highly competitive sector.

· Acquisitions: It may be the case that the acquisitions made are not successful or are purchased at inappropriate prices.

PEERS AND VALUATION

It´s complicated to find a company with the same characteristics and business lines as Creightons. The following table shows some data of listed companies belonging to beauty sector. As we can see, big players have historically traded at higher multiples than Creightons, despite having no or limited growth, which is logical given higher brand recognition, better margins, economies of scales and size. Currently, CRL is trading around 10 P/FCF FY21 with good prospects, strong financials and a capable management, an interesting valuation in my honest opinion.

We present two scenarios (Base and Bear case) to estimate the future value of the company.

Base Case:

· Stock price 25/02/2022: 0,70 GBP

· The company meets the strategic plan: 100M sales in 2024 and 12,5 M EBITDA

· 20M growth through M&A financed by share issuance and debt and 20M through organic growth.

· Tax rate 19%

· Multiples: 15x P/FCF and 10x EV/EBITDA.

· Target Price 2024: 1,55 GBP (30% CAGR)

Bear Case

· Stock price 25/02/2022: 0,70 GBP

· The company does not meet the strategic plan: 75M sales in 2024 and EBITDA margin below 12%.

· Tax rate 19%

· Múltiples: 12x P/FCFx and 7x E/EBITDA

· Target Price 2024: 0,9 GBP (8,7% CAGR).

DISCLAIMER: This communication does not constitute a recommendation to buy, sell, or hold any investment securities. Do your own due dilligence.